The previous blogs have covered both the basic and niche requirements for tax depreciation in the US. I’m going through even more niche and industry-specific requirements and trying to determine if a given topic is really worth blogging about. One that I remembered that should definitely be covered is the US requirement for US passenger vehicles. Let’s dive into it!

Blog Series:

Handling US Tax Depreciation in SAP (Part 1): The Basics

Handling US Tax Depreciation in SAP (Part 2): Separate Books

Handling US Tax Depreciation in SAP (Part 3): Basis Adjustments

Handling US Tax Depreciation in SAP (Part 4): Prior Year Adjustments

Handling US Tax Depreciation in SAP (Part 5): Mid-Period and Mid-Quarter Convention

Handling US Tax Depreciation in SAP (Part 6): IRS Passenger Vehicles

Handling US Tax Depreciation in SAP (Part 7): Tax Forms 4562 & 4797

Separate Rules for What?

For all of the normal capital equipment that a company can put on it’s balance sheet, the IRS generally depreciates them using the same set of conventions. Double declining, 150% declining, straight line, or no depreciation at all. Bonus or no-bonus. The math behind them isn’t too complex, and quite frankly, it wouldn’t matter if it was because the IRS publishes various schedules that show the applicable depreciation rates to use. Knowing how the rates are determined helps when analyzing issues in SAP but it’s not required for a basic understanding of US tax.

But wait, aren’t there already rules around depreciation for vehicles? Yes, of course there are but if it’s a passenger vehicle (car, truck, or electric vehicle) it gets depreciated differently. The key word here is ‘passenger’. These aren’t vehicles used for operational purposes. If it’s a large truck that delivers product or used in a manufacturing environment, then it’s a piece of equipment and depreciates over 5 years. We all know that most cars/trucks last well beyond 5 years but the IRS allows an accelerated depreciation convention for that type of equipment.

But if it’s used solely for passengers, then it has it’s own depreciation schedule which is not nearly as lenient. This specification was created because back in the 1980’s (and earlier) corporations would provide company cars to managers or salespeople. This was usually a form of compensation which started to complicate payroll tax and the whole personal vs. corporate tax divide. As a result, the IRS decided on a different (and far more conservative) depreciation schedule for these types of vehicles to curb the practice. US companies now don’t engage in this nearly as much as they use to but it’s still done and has to be tracked differently.

What’s the Requirement?

You can read the specifics about the regulation in the IRS publication but here is a quick screenshot of the annual calculation limits up through 2017.

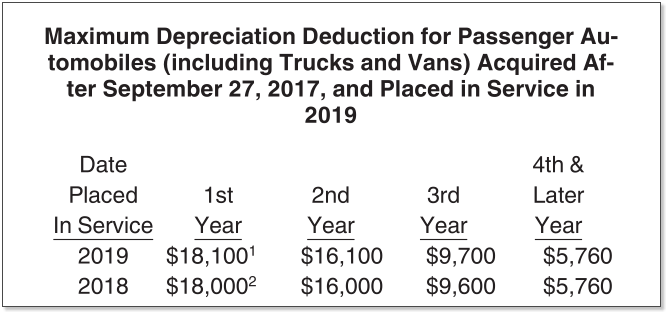

Here are the newer figures for 2018-2019. They haven’t published the new values for 2020 yet but the changes will most likely be the same or have minor changes from the 2019 figures.

To summarize the above tables, the amounts that the IRS allows to depreciate basically operate on a 4 year schedule. Using 2019 (the most current year) as an example, no matter how much the asset was purchased for, you are only allowed to depreciate up to $18,100 in the first year, and this $18,100 is considered as bonus depreciation. If the vehicle was cheap enough and was under this number, then you could immediately reclaim all of it via depreciation but that’s rarely the case. In year 2, you can depreciate up to a maximum of $16,100. Year 3 is limited to $9,700 and year 4 onwards allows a maximum of $5,760 until the vehicle is fully depreciated.

Here’s an example. Let’s say Company XYZ purchases a new vehicle for their CEO that costs $88,500. The depreciation for a normal 5 year MACRS DDB asset would be as follows:

But because the asset is a passenger vehicle, it should depreciate differently as the table below shows.

But wait! I forgot about bonus depreciation! The final depreciation schedule for this asset should technically be calculated in SAP as shown below.

How Does the IRS Come Up With These Rates?

Honestly, I don’t know because the IRS doesn’t state how the numbers are calculated as they do with the accelerated approach (i.e., double-declining) for the normal tax tables. I’m not saying it’s arbitrary but the curve that comes out of this isn’t a steep one; it’s actually quite linear in nature. The IRS is extending (dragging out) the time frame to recover the purchase price and in this way discourage companies from making these kind of purchases.

Looking at the tables shown above you can see that how those figures spread out especially if the initial APC of the asset is large. Instead of always depreciating over 6 calendar years, it could take up to 11. But again, they don’t explain how the $10,960 figure for 2008 capitalizations was calculated.

Let’s See it in SAP

Here is an asset with the same figures from above. The year 1 depreciation is capped at the $18,100 amount and is shown as special depreciation. The following years are also the same as the IRS schedule from above and classified as ordinary depreciation, until the asset is fully recovered in year 11 (2030).

What Makes This Difficult?

As usual, this comes down to the proper configuration in the subledger to support it. There are some master data issues at the asset class level but only if you are tracking different types of passenger vehicles. I rarely see issues with the capitalization process for this requirement or any niche reporting issues… it’s just configuration that has to be worked out.